Birmingham Area MLS* Monthly Observations for March 2017

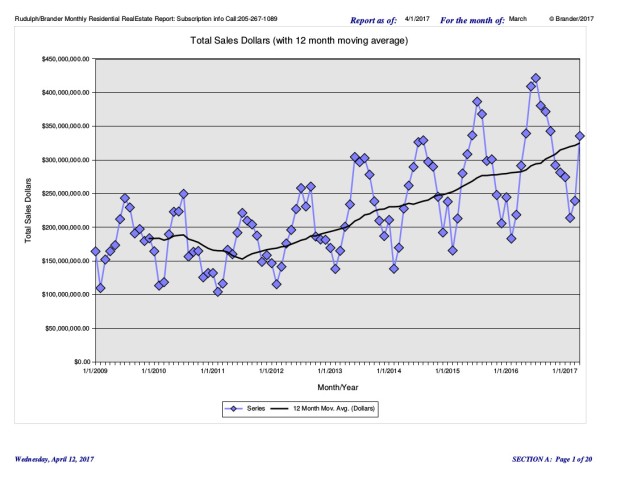

March saw an acceleration of the uptick in dollar and unit sales over last year. Prices seem to be modestly increasing. Total dollar sales for March were $335,608,193 up 15% from $291,558,899 last year, and up 40% from last month at $239,312,908.

Total Unit sales were up 6% at 1,629 in March from 1,530 last year and up by 35% compared with 1,204 in February. New sales were off at 150 homes this month, vs. 155 in February, and off by 30 from 175 last year. The low inventory level of new homes suggests a good environment for builders, and prices have begun to show a more solid uptrend. Used sales were 1,479 homes in March, up 41% from 1,049 last month, and up by 9% from 1,355 last year (Sect E p.3).

ACRE numbers are slightly different from those we report. For ACRE, our month by month 2017 forecast can be seen here: ACRE. For Birmingham, the full year projection for 2017 = 15,238, a 3.6% difference from 2016 actual of 14,705. The cumulative error is minus 1% for the year; that is actuals are behind projections of 3,200 through March, at 3,162 actual thru March.

Total inventory is slightly higher this month at 8,150 vs. last month at 7,851 and less than 9,313 last year. (Sect C p.1). Active New listings decreased to 997 in March from 1,067 in February (Sect E p.3). Absorption rate for New homes is at 6 months supply this month, which is less than 7 months last year. (Sect E p.3). The New homes have normal inventory levels in the 4-8 month range depending on area and price range. (Sect C p.1).

Absorption for Used homes in March shows 5 months, which is less than the 6 last year. Used Active listings at 7,153 are up from last month of 6,784, and less than 8,228 last year (Sect E p.3). Inventory levels have continued to trend down from prior years. Market performance is highly area specific, so check the individual area charts. For instance, Mountain Brook has between 1 and 6 months of inventory, 4 months overall, except in the $5-$600,000 and over $900,000 category, which each have 6 months of inventory. In the over $900,000 price range there were 40 homes, with 9 sold in that price range last month. There are a number of MLS areas, particularly those known as the “over the mountain” communities, showing similarly low levels, including Homewood, which has 4 months of inventory.

Birmingham area Average Days on Market for New houses is 239 compared with last month at 197. The Used homes DOM was 115 in March vs 125 last month, (Sect A p.18). Average sales price for Sold New homes decreased to $276,271 from $288,821 last month (Sect A p2). Over a several month period prices seem to be increasing. Average sales price for Sold Used was $198,896 this month compared to $185,458 last month. (Sect A p2).

All in all, the market continues to look quite healthy.

TWB 4/12/2017